April Single-Family Home Prices Up 0.5 Percent

Oxford, Miss. (June 22, 2011) – FNC announced Thursday that U.S. home prices continue to show notable improvement in April. Despite broad economic and job market weakness, home prices have increased for the first time since the withdrawal of the homebuyer tax credits a year ago.

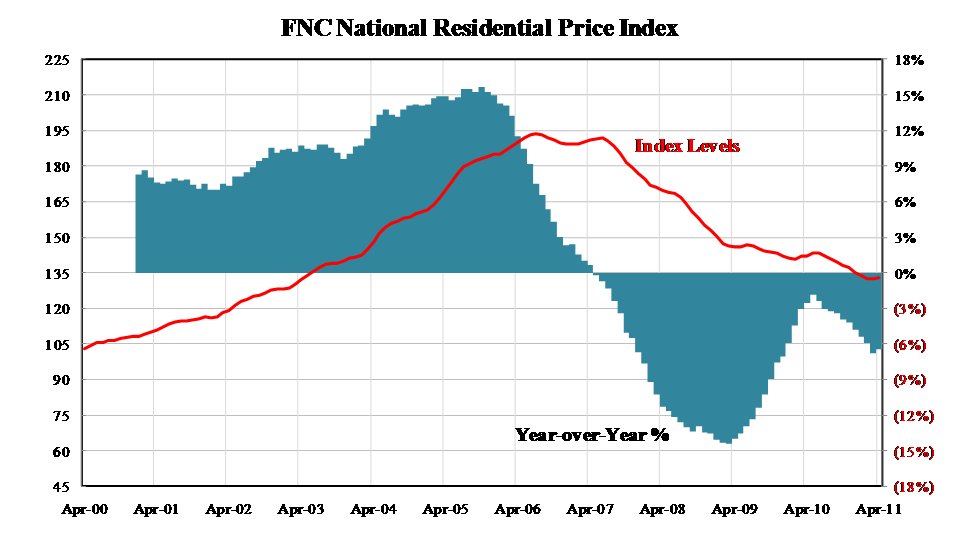

Based on the latest data on non-distressed home sales (existing and new homes), FNC’s Residential Price Index™ [1] (RPI) indicated that single-family home prices in April were up from March at a seasonally unadjusted rate of 0.5%. Despite downward price pressure from high volumes of foreclosure sales, home prices continue to gain traction in April after remaining relatively unchanged in March.

Contrary to recent reports of continued price deteriorations, FNC’s RPI – the industry’s first hedonic price index built on a comprehensive database blending public records with real-time appraisals of property and neighborhood attributes – shows that underlying home value appears to be stabilizing.[2] With distressed properties making up as much as a third of total home sales, a significant portion of observed price declines can be attributed to deteriorating conditions typically associated with foreclosed properties (e.g., poor maintenance, theft, vandalism). Because of these and other hidden costs, as well as risk and stigma associated with buying foreclosed properties – not necessarily fundamental declines in home value – buyers can often expect large discounts priced into foreclosure sales. Considering foreclosure price discounts as part of the changes in fundamental home value could render quite different conclusions about recent market developments or its near-term outlook.

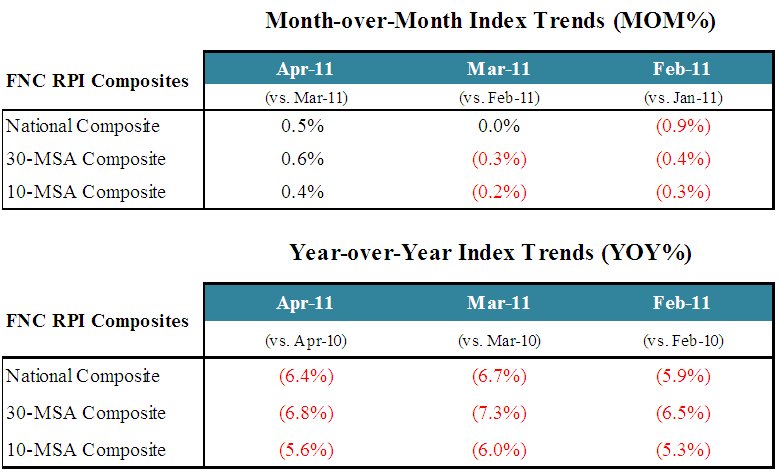

All three RPI composites (the National, 30-MSA, and 10-MSA indices) showed a modest uptrend in April, ranging from 0.4% by the 10-MSA composite to 0.6% by the 30-MSA. Nationwide, home prices rose 0.5% between March and April. On a year-over-year basis, home prices nationwide are 6.4% below the levels attained a year ago.

Within the 30-MSA composite index, home prices moved higher in 17 markets at an average rate of 2.5%. This is a marked improvement over March in which only 13 markets experienced higher prices from the previous month. Of the remaining 13 falling markets, the average rate of price decline was 1.3%.

A number of markets have moved up modestly since the start of 2011: Houston 6.6%, Charlotte 4.5%, Minneapolis 4.0%, San Antonio 2.7%, Washington D.C. 2.6%, San Diego 2.3%, and Portland 1.9%. Orlando, on the other hand, leads the nation in home price declines during 2011–having lost more than 4.0% in the last four months, followed by Riverside, California at -3.2%, Baltimore and New York at -2.5%, Dallas -2.3%, Atlanta -2.1%, and Phoenix and Las Vegas at -1.8%.

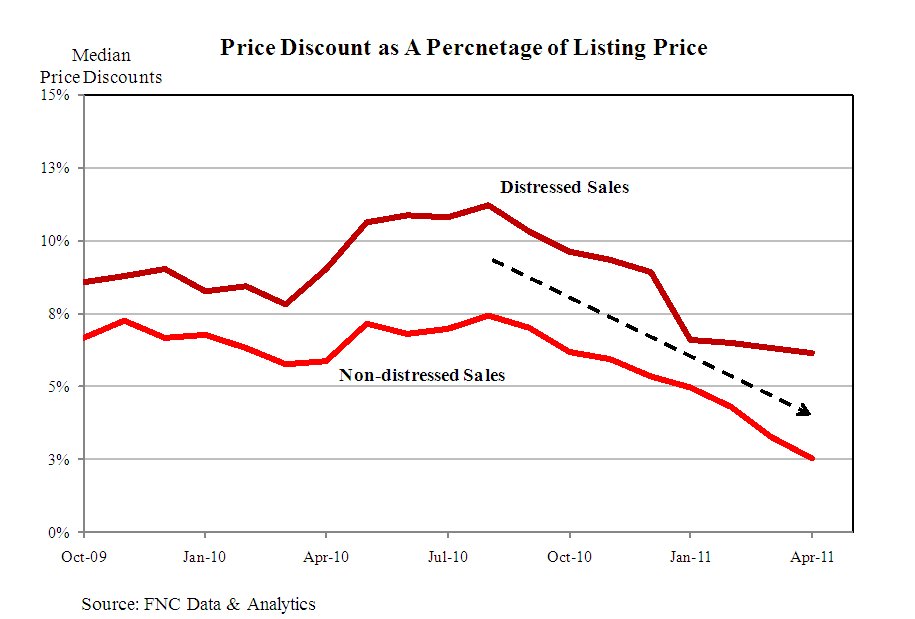

Consistent with improving home price trends are improved market liquidity in recent months. First, there has been a rapid increase in recent months in the number of homes listed for sale. Since December, listing activities have increased more than 65% – with the arrival of spring/summer home buying season and despite decelerations in foreclosure rates. Secondly, the overall listing price discounts – the percentage difference between the initial listing price and final sale price – have dropped from 6.7% in Q4 2010 to 4.0% in Q1 2011. Finally, listing properties’ time-on-market is trending down. Median time-on-market for non-distressed listing has decreased from four months in October 2010 to 2.5 months in April.

Moreover, the improvement of market liquidity is seen in both distressed and non-distressed market segments. For non-distressed sales, listing price discounts fell from 5.0% in January to 3.0% in April; in distressed sales (inclusive of short sales, REOs, and foreclosed properties), the listing price discount decreased from 7.0% in January to 6.0% in April and continues to decline.

[1] The FNC National Residential Price Index is a volume-weighted aggregate price index consisting of 100 major metropolitan areas across different regions of the U.S. All FNC Residential Price Indices are constructed to capture unsmoothed home price trends in the underlying housing market that excludes foreclosed properties.

[2] Detailed, real-time appraisal data is used to measure property and neighborhood attributes used in the hedonic model to control for their impact on home prices. No appraisal value is used in the index estimation, however.

Contact:

Bill Dabney, FNC PR Manager

Phone 662/236.8304

bdabney@fncinc.com

www.fncinc.com

Tags: