Fashion e-commerce: current growth is driven by successfully attracting new consumers

AMSTERDAM – 15th June 2020 | AfterPay Insights’ research has shown that Fashion has increased overall since end of March. What are the drivers of growth? And how satisfied are consumers? Which dimensions do Fashion merchants need to navigate in the new e-commerce landscape of today?

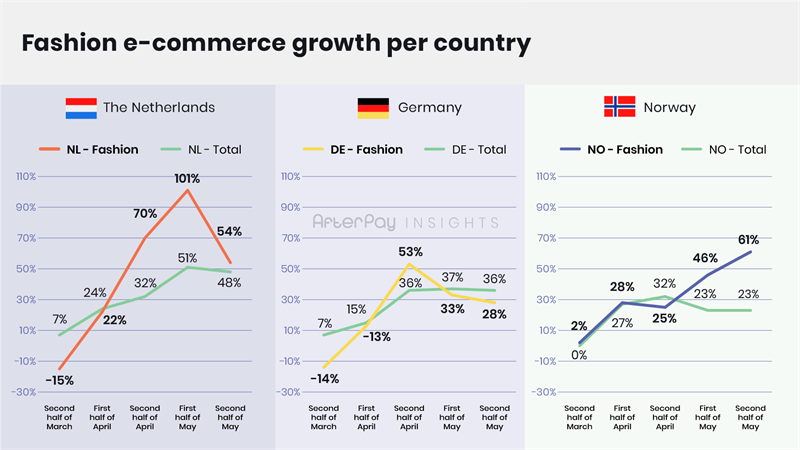

Since end of March, AfterPay Insights has conducted weekly interviews with now 16.500 consumers in The Netherlands, Germany and Norway about their changing e-commerce behavior. Fashion has grown significantly in all three countries, with e-commerce purchases in The Netherlands up +54%, in Germany up +28% and in Norway up +61%.

The results show that there are two key drivers for the recent growth in Fashion e-commerce. First, online Fashion merchants have succeeded in attracting consumers who previously purchased Fashion offline. The share of online shoppers who have purchased in Fashion during a two-week period has grown steadily from 18% to 28% in The Netherlands, from 18% to 25% in Germany and from 14% to 20% in Norway. A result is that the socio-demographic profile of online Fashion Shoppers has broadened, now also encompassing relatively more males and families with kids, as well as consumers living in city suburbs and mid-sized towns.

Second, existing Fashion Shoppers make more online purchases, leading to a slight increase in Fashion e-commerce volume. Across all countries, Fashion Shoppers have done between 1,3 and 2,2 Fashion purchases during a two-week period. This fluctuation is likely due to different timings, such as timing of summer Fashion sales across the different countries as well as the fact that different countries are easing corona restrictions.

AfterPay Insights’ research also shows that Fashion Shoppers conduct twice as many online purchases compared to non-Fashion Shoppers. A Fashion shopper typically makes 50% of their purchases within Fashion; the other 50% is distributed among all other e-commerce categories.

‘Heavy’ and ‘Medium’ Fashion Shoppers stand for 65% of online Fashion purchases

Different types of shoppers exist when looking at shopping frequency per two weeks: Heavy Fashion Shoppers make 4+ online fashion purchases, Medium Fashion Shoppers make 2-3 online fashion purchases and Light Fashion Shoppers make 1 online fashion purchase.

A relatively small number of consumers is driving the growth of online fashion purchases. ‘Heavy Fashion Shoppers’ stand for about 25% of all online Fashion purchases, and ‘Medium Fashion Shoppers’ account for about 40% of purchases. This means that Heavy and Medium Fashion Shoppers as a group represent 10% of all online shoppers in the population, and stand for 65% of all Fashion purchases.

Looking at Heavy Fashion Shoppers specifically, these conduct around 70% of all their online purchases within Fashion. The corresponding figure among Medium Fashion Shoppers is around 50% and among Light Fashion Shoppers 37%.

Fashion shoppers are slightly more demanding

A pattern that is consistent across The Netherlands, Germany and Norway is that Fashion shoppers have a significantly higher demand on merchants when it comes to flexible return options. Even though this is not the biggest need (only 15-20% of Fashion Shoppers express this as important), it is overall the 6th most important demand that these shoppers place on merchants.

In The Netherlands, aside from flexible return options, Fashion shoppers here also express a higher need regarding flexible payment options.

Fashion shoppers in Germany really differentiate themselves regarding flexible return options, as the difference between ‘all shoppers’ and Fashion shoppers regarding this aspect is quite dramatic.

In Norway, Fashion shoppers do not only demand more flexible return options and more flexible payment options, but they also are more price sensitive looking for lowest price websites to a higher extent than the average online shopper.

Consumers are least satisfied with logistics and customer service

Compared to the average online shopper, Fashion Shoppers are overall significantly more satisfied with the ‘return process’, even though this also is the one area where Fashion shoppers have higher expectations. But on the other hand, Fashion shoppers are generally less satisfied with Fashion merchants when it comes to shipping & delivery (incl. fast delivery time) as well as customer service.

In The Netherlands, Fashion shoppers are less satisfied with Fashion merchants ‘shipping & delivery (incl. fast delivery time) compared to the general online shopper satisfaction with this aspect. But Dutch Fashion shoppers are significantly more satisfied with Fashion merchants’ return process and Heavy/Medium Fashion shoppers are significantly more satisfied with Fashion merchants’ having products in stock.

German Fashion shoppers rate the satisfaction with their Fashion purchases in the basic same way as Dutch Fashion shoppers, i.e. lower scores compared to the average shopper on shipping and fast delivery and a relatively higher satisfaction with the return process. The difference being that German Fashion shoppers are less satisfied with Fashion merchants’ having products in stock. Also, the general level of Fashion merchant satisfaction is lower among Fashion shoppers in Germany compared to in the Netherlands.

And what stands out in Norway is that Fashion shoppers are relatively more satisfied with the return process and at the same time relatively less satisfied with customer service. Also, the satisfaction gap between Heavy/medium Fashion shoppers and Light Fashion shoppers is large in Norway, i.e. Light Fashion shoppers in Norway are very satisfied in general – with the exception of the area of customer service.

How will Fashion e-commerce develop?

We see significant changes in consumers’ e-commerce behavior in Fashion over the past months and we can partly connect these to the global pandemic. Still there are other perspectives when looking ahead. First of all, seasonality is a hugely important factor when looking at Fashion. Second, as lockdowns are eased and society opens up, visits to and sales in brick-and-mortar Fashion stores are likely to pick up again. Another result of lighter restrictions will also result in increased travel, a factor that is likely to influence Fashion (e-commerce) as well. A looming economic crisis – and increasing unemployment rates - will potentially erode consumer confidence and lead to cuts on spending. And with Fashion’s discretionary nature, the industry is particularly vulnerable here. Finally, as some consumers change their lifestyle and shift priorities, consumers’ attitudes about their general consumption levels may change.

AfterPay Insights will continue this research throughout the summer, in order to follow developments and will get back with an updated report after the summer.

View the interactive dashboard with consumerdata and insights.

About AfterPay Insights

AfterPay Insights is a knowledge platform for e-commerce professionals. From mid March, AfterPay Insights has researched consumers’ e-commerce behavior during the corona outbreak and intend to continue this study through out the pandemic. This article is an abstract.

About AfterPay

AfterPay, developed by Arvato Financial Solutions is the biggest payment-after-delivery service in The Netherlands and Belgium, and is also available in Germany, Austria, Switzerland, Sweden, Norway, Finland and Denmark.

About Arvato Financial Solutions

As part of Bertelsmann, Arvato Financial Solutions provides professional credit management solutions across all segments of the customer lifecycle in around 20 countries. By revealing the advantages of predictive analytics, leading-edge platforms and big data, provided solutions result in optimized financial performance and empower clients to fully concentrate on their core business.

Research contact

Aida Beelaerts van Blokland

a.beelaertsvanblokland@afterpay.nl

+31 6 57 32 10 95

Tags: