FNC Study: How Local Market Conditions Affect Appraisal Valuations

Last month, the Appraisal Institute released “Guide Note 12: Analyzing Market Trends,” a resource designed to give AI members an analytical framework for studying market trends while developing a market value opinion on a property. The Guide Note is particularly concerned with challenges faced by appraisers when market conditions are rapidly changing, as demonstrated by recent boom and bust cycles of the U.S. housing market. In slower markets like today’s, the Guide Note recognizes that a lack of market data is challenging to appraisers attempting to make market value adjustments.

Indeed, appraisers commonly face such challenges and more in today’s markets. Underlying market conditions are far from stable; continued downtrends in home prices often require appraisers to apply appropriate market trend adjustments to recent comparable transactions. Moreover, in many distressed markets it is also likely that some or all available recent transactions are distressed sales. Since the parties to distressed properties are often unique and distressed properties are typically sold at a significant price discount, which may or may not represent underlying market trends, appraisers are challenged with deciding whether such distressed sales are relevant market data for non-distressed transactions or whether adjustments are needed to better extract relevant market information.

In this report, we use a large dataset of recently completed purchase-mortgage appraisals to analyze how appraisal valuations respond to local market conditions, particularly when conditions are prone to produce less efficient transaction prices. It is well known that buyer-seller-negotiated prices can deviate from a property’s market value due to various inefficiencies that exist in real estate transactions. The problem is compounded by distressed conditions that characterize many local markets. It will be generally more difficult to obtain relevant price information in distressed, inactive markets. More actively traded markets, on the other hand, make it easier to observe relevant price information and market trends ─ more likely to result in a more efficient price outcome for the buyer and seller and thus less likely that the appraisal value will deviate much from the observed price.

Our results show that appraisal value can differ quite significantly from contract price despite the fact that nearly one in three pre-closing sales transactions appraise at exactly the contract price. Of a sample of purchase-mortgage appraisals on single-family homes and condominiums completed between January and May 2012, about 24% are appraised above contract by 3.0% or more. Combined with another 8-9% appraised at below contract by 3% or more, nearly a third of the purchase-loan appraisals contain a market value opinion differing at least 3% in value from the contracts.

More importantly, our results show that appraisal valuation appears to be performing the important risk management function it is designated to do for lenders’ mortgage transactions: helping to ascertain the fair value of the underlying collateral. Our data reveal a strong positive correlation between indications of market inefficiency and appraisal valuation’s tendency to move away from a contract price; when underlying market conditions are more inclined to produce less efficient transaction prices, there is a greater chance that appraisal value will deviate from the contract price. A statistical probability model is used to analyze how market conditions affect the likelihood that a significantly different appraisal value will be observed. In this study, a significantly different appraisal valuation is defined as one in which appraised value falls below or above contract by at least 3% of contract price.

- More active markets – defined in this study as having at least 10 non-distressed sales in a prior month – are associated with lower probability of observing significantly different appraisal valuation. A more active market makes gleaning information more efficient.

- Greater market distress – measured by the proportion of distressed properties in total homes sales in the prior three months – is associated with a higher probability that a significantly different appraisal valuation will be observed. More specifically, market distress increases the probability of appraisal valuation falling significantly below the contract price.

- REO or short sale properties are more likely to be appraised at higher value than the contract price. Sellers of such properties are driven to make a quick sale and are typically willing to ask a price significantly below the property’s fair market value in exchange for liquidity.

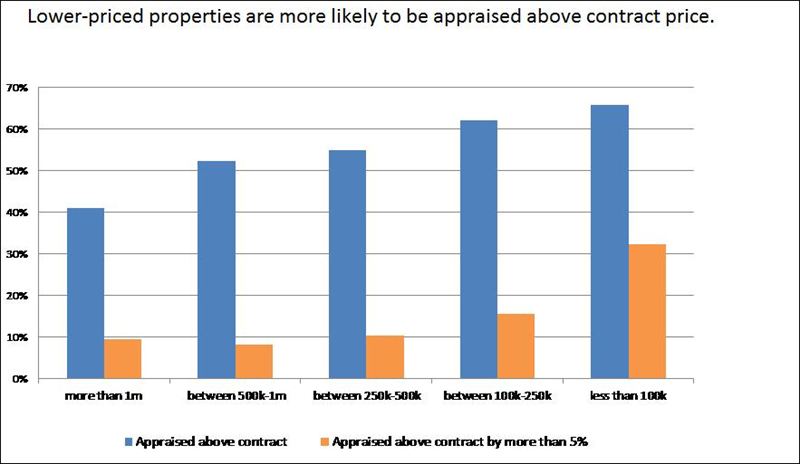

- Low-tier properties – contract price below $250,000 – are more likely to be appraised above the contract price. [1] In contrast, high-tier properties (those with a contract price at $1 million or more) are less likely to receive a higher valuation. Since the subprime mortgage crisis is concentrated among low-tier properties, distressed sales are more likely to occur among these properties as their owners fall into financial distress. The short sale is an example of this trend. Since the data we analyze often has missing information regarding a property’s distressed sale status (short sale, REO, or other forms of distress), we suspect the low-tier property indicator picks up such impact on appraisal valuation.

However, market-based appraisals have often been criticized for failing to support potential mortgage transactions – especially if the adjustments result in a lower appraised value than the contract price. Our analysis reveals appraiser due diligence in the process of developing a market value opinion on the underlying collateral. Meanwhile, we find the majority of appraisals provide a valuation that supports the contract price. As shown below, the evidence does not support the claim that low appraisal valuation has prevented contract closings.

[1] According to a newly released report from the General Accounting Office, “Residential Appraisals: Regulators Should Take Actions to Strengthen Appraisal Oversight,” the nation’s five largest lenders obtained appraisals for 98% of home purchase mortgages sold to the GSEs or insured by FHA.

To interview any of FNC’s mortgage industry experts, contact:

Bill Dabney, manager of public relations

FNC, Inc.

Phone 662/236.8304

bdabney@fncinc.com

About FNC, Inc.

Since 1999, FNC has pioneered real estate information technology, automated appraisal ordering, tracking, documentation and review for lender and servicer compliance with government regulations. FNC’s platforms are in production at seven of the 10 largest U.S. mortgage lenders and provide value to large and small lenders with reduced costs and more efficient loan processing. With collateral management platforms, data and analytics, FNC provides advanced insight into the property backing a loan from origination to capital markets. Visit FNC online at www.fncinc.com.

Tags: